2026 IRA Contribution Limits: Your Complete Guide to Traditional, Roth, and SIMPLE IRA

The IRS has announced significant updates to retirement account contribution limits for 2026, bringing welcome news for savers looking to maximize their tax-advantaged retirement savings. Whether you contribute to a Traditional IRA, Roth IRA, or SIMPLE IRA, understanding these changes is essential for optimizing your retirement strategy in the year ahead.

Traditional IRA and Roth IRA: 2026 Contribution Limits

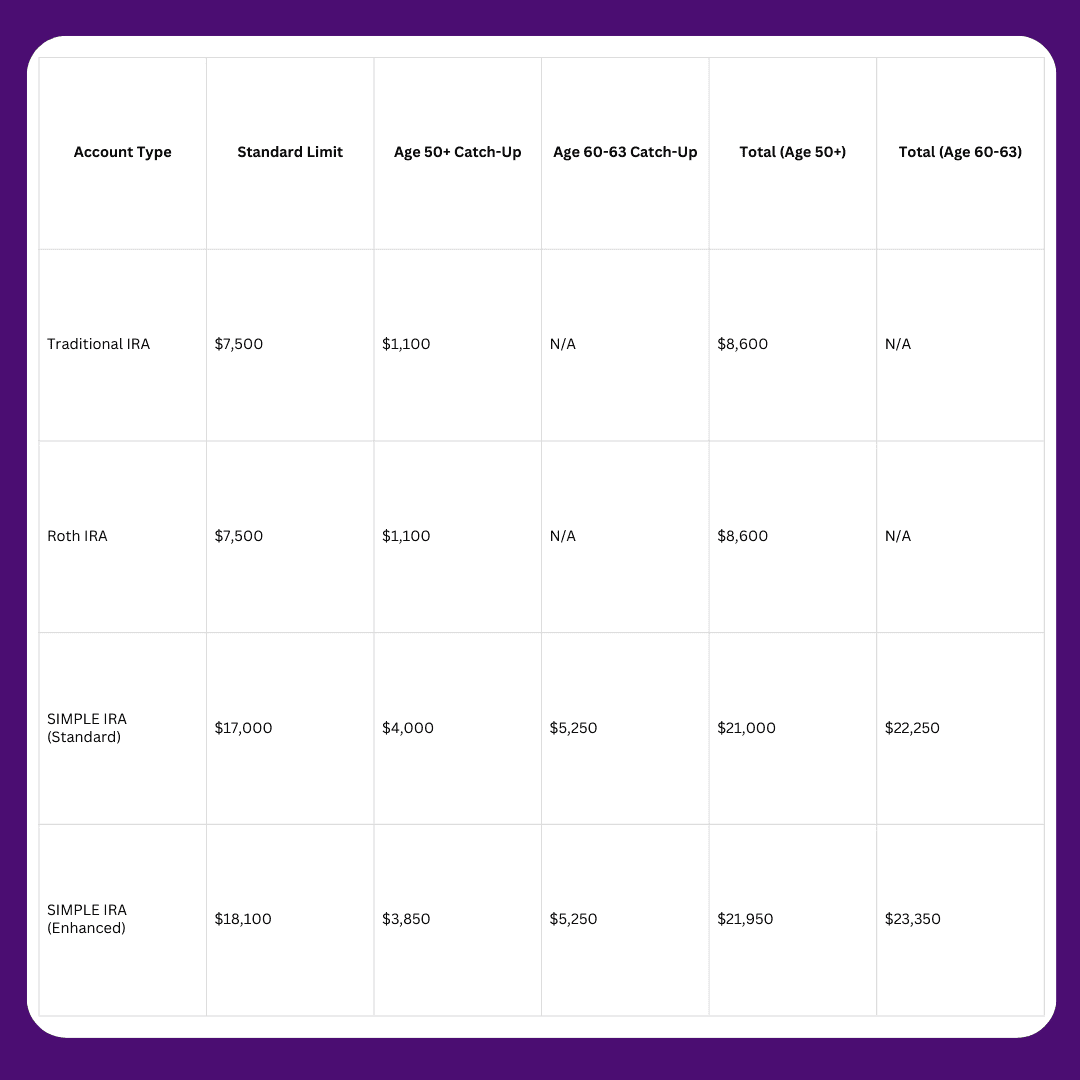

For 2026, the annual contribution limit for both Traditional IRAs and Roth IRAs has increased to $7,500, up from $7,000 in 2025. This $500 increase represents another meaningful step forward in helping Americans build their retirement savings.

Understanding the Combined Contribution Limit

Important: The $7,500 limit is your total combined contribution across all Traditional IRA and Roth IRA accounts you own. This is a cumulative limit, not a per-account limit.

For example, you could:

- Contribute $7,500 to a Traditional IRA and $0 to a Roth IRA

- Contribute $4,000 to a Traditional IRA and $3,500 to a Roth IRA

- Contribute $0 to a Traditional IRA and $7,500 to a Roth IRA

Any combination is acceptable as long as your total contributions across all Traditional and Roth IRA accounts do not exceed $7,500 for the year.

Catch-Up Contributions for Traditional and Roth IRAs

If you're age 50 or older, you can take advantage of enhanced catch-up contributions. For 2026, the catch-up contribution limit for Traditional IRAs and Roth IRAs has increased to $1,100, up from $1,000 in 2025. This means individuals age 50 and over can contribute a total of $8,600 to their Traditional IRA or Roth IRA in 2026.

These catch-up provisions were amended under the SECURE 2.0 Act of 2022 to include annual cost-of-living adjustments, ensuring that contribution limits keep pace with inflation over time.

Traditional IRA Deductibility: Understanding the 2026 Phase-Out Ranges

While contribution limits apply equally to Traditional IRAs and Roth IRAs, the tax treatment differs significantly between them. Traditional IRA contributions may be tax-deductible depending on your income, filing status, and whether a workplace retirement plan covers you or your spouse.

When Traditional IRA Deductions Phase Out

Suppose you or your spouse participates in a workplace retirement plan such as a 401(k), 403(b), or 457 plan. In that case, your ability to deduct Traditional IRA contributions may be reduced or eliminated based on your modified adjusted gross income (MAGI). Here are the 2026 Traditional IRA deduction phase-out ranges:

Single Taxpayers Covered by a Workplace Plan:

- Phase-out range: $81,000 to $91,000

- Increase from 2025: $79,000 to $89,000

If you're a single filer with a MAGI between $81,000 and $91,000, your Traditional IRA deduction will be partially reduced. Once your income exceeds $91,000, you cannot deduct Traditional IRA contributions if a workplace retirement plan covers you.

Married Filing Jointly (Contributor Covered by Workplace Plan):

- Phase-out range: $129,000 to $149,000

- Increase from 2025: $126,000 to $146,000

For married couples filing jointly where the spouse making the Traditional IRA contribution is covered by a workplace plan, the deduction phases out between $129,000 and $149,000 of combined MAGI.

Married Filing Jointly (Contributor NOT Covered, Spouse IS Covered):

Phase-out range: $242,000 to $252,000

Increase from 2025: $236,000 to $246,000

If a workplace retirement plan does not cover you but your spouse is, you can still deduct your Traditional IRA contributions up to a much higher income threshold. The spousal Traditional IRA deduction phases out between $242,000 and $252,000.

Married Filing Separately (Covered by Workplace Plan):

- Phase-out range: $0 to $10,000

- No change from 2025

This phase-out range is not subject to annual cost-of-living adjustments and remains unchanged.

Important Note About Traditional IRA Deductibility

If a workplace retirement plan covers neither you nor your spouse, you can deduct the full Traditional IRA contribution regardless of your income level. The phase-out ranges only apply when workplace plan coverage exists.

Roth IRA: Understanding the 2026 Income Limits

Unlike Traditional IRAs, Roth IRA contributions are never tax-deductible. However, qualified withdrawals from a Roth IRA in retirement are completely tax-free, making them an attractive option for many savers. The trade-off is that Roth IRA contribution eligibility is based solely on income, regardless of workplace plan participation.

2026 Roth IRA Income Phase-Out Ranges

Single Filers and Heads of Household:

- Phase-out range: $153,000 to $168,000

- Increase from 2025: $150,000 to $165,000

If you're single or file as head of household with a MAGI between $153,000 and $168,000, your Roth IRA contribution limit will be reduced. Once your income exceeds $168,000, you cannot contribute directly to a Roth IRA.

Married Filing Jointly:

Phase-out range: $242,000 to $252,000

Increase from 2025: $236,000 to $246,000

For married couples filing jointly, the Roth IRA contribution phase-out ranges from $242,000 to $252,000 of combined MAGI.

Married Filing Separately:

- Phase-out range: $0 to $10,000

- No change from 2025

If you're married, filing separately, the Roth IRA income phase-out range remains $0 to $10,000 and is not subject to annual adjustments.

Roth IRA Strategy Considerations

High earners who exceed the Roth IRA income limits may want to explore the "backdoor Roth IRA" strategy, which involves making non-deductible Traditional IRA contributions and then converting them to a Roth IRA. Consult with a tax professional to determine if this strategy is appropriate for your situation.

SIMPLE IRA: 2026 Contribution Limits for Small Business Employees

SIMPLE IRAs (Savings Incentive Match Plan for Employees) are retirement plans designed for small businesses with 100 or fewer employees. These plans have their own contribution limits that differ from those of Traditional and Roth IRAs. Like Traditional IRA contributions, SIMPLE IRA contributions are made with pre-tax dollars, reducing your taxable income in the year you contribute.

Standard SIMPLE IRA Contribution Limits

For 2026, the amount individuals can contribute to a SIMPLE IRA has increased to $17,000, up from $16,500 in 2025. This represents a $500 increase that allows small business employees to save more for retirement.

Enhanced SIMPLE IRA Contribution Limits

Thanks to changes made in the SECURE 2.0 Act, specific qualifying SIMPLE IRA plans can now accept higher contribution amounts. For 2026, this enhanced SIMPLE IRA contribution limit has increased to $18,100, up from $17,600 in 2025.

Your employer's SIMPLE IRA plan must meet specific requirements to qualify for this higher limit, so check with your plan administrator to confirm which limit applies to your situation.

SIMPLE IRA Catch-Up Contributions for Ages 50 and Over

Employees age 50 and older participating in a SIMPLE IRA can make additional catch-up contributions. For 2026, the standard SIMPLE IRA catch-up contribution limit has increased to $4,000, up from $3,500 in 2025.

For those participating in an enhanced SIMPLE IRA plan, a different catch-up limit applies. This enhanced SIMPLE IRA catch-up contribution limit remains at $3,850 for 2026.

This means individuals age 50 and over can contribute:

- $21,000 total to a standard SIMPLE IRA ($17,000 + $4,000 catch-up)

- $21,950 total to an enhanced SIMPLE IRA ($18,100 + $3,850 catch-up)

Special SIMPLE IRA Catch-Up for Ages 60 to 63

The SECURE 2.0 Act introduced an even higher catch-up contribution limit for employees in a specific age range. For 2026, employees aged 60 to 63 participating in a SIMPLE IRA can make catch-up contributions of up to $5,250, unchanged from 2025.

This special provision allows those approaching retirement to accelerate their SIMPLE IRA savings during these critical years. Individuals in this age bracket can contribute:

- $22,250 total to a standard SIMPLE IRA ($17,000 + $5,250 catch-up)

- $23,350 total to an enhanced SIMPLE IRA ($18,100 + $5,250 catch-up)

The Saver's Credit: Additional Tax Benefits for IRA Contributors

Beyond the direct tax benefits of Traditional IRA deductions and Roth IRA tax-free growth, eligible low and moderate-income workers may qualify for the Retirement Savings Contributions Credit, commonly known as the Saver's Credit.

This valuable tax credit can be worth up to 50% of your contributions to a Traditional IRA, Roth IRA, or SIMPLE IRA, depending on your adjusted gross income and filing status.

2026 Saver's Credit Income Limits

Married Filing Jointly:

- Income limit: $80,500

- Increase from 2025: $79,000

Head of Household:

- Income limit: $60,375

- Increase from 2025: $59,250

Single or Married Filing Separately:

- Income limit: $40,250

- Increase from 2025: $39,500

If your income falls below these thresholds, you may qualify for this credit in addition to any Traditional IRA tax deduction. The Saver's Credit applies to contributions to Traditional IRAs, Roth IRAs, and SIMPLE IRAs, as well as to 401(k) and other workplace retirement plan contributions.

2026 IRA Contribution Limits at a Glance

Now that you understand the details, here's a quick reference table summarizing all 2026 IRA contribution limits:

*Note: Traditional and Roth IRA limits are combined totals across all your IRA accounts.

Strategic Planning for 2026: Maximizing Your IRA Contributions

Understanding these 2026 limits is just the first step. Here are strategic considerations for each IRA type:

Traditional IRA Strategy

Traditional IRAs are best suited for individuals who expect to be in a lower tax bracket during retirement than they are currently. If you're currently in a high tax bracket and qualify for the Traditional IRA deduction, the immediate tax savings can be substantial. Consider maxing out your Traditional IRA contributions if:

- Your income falls below the deduction phase-out ranges

- You're in a higher tax bracket today than you expect to be in retirement

- You want to reduce your current taxable income

Roth IRA Strategy

Roth IRAs are ideal for individuals who expect to be in the same or a higher tax bracket during retirement. While Roth IRA contributions don't provide an immediate tax deduction, the tax-free growth and tax-free withdrawals in retirement can be incredibly valuable. Consider prioritizing Roth IRA contributions if:

- Your income allows for Roth IRA contributions

- You're early in your career with room for income growth

- You want tax diversification in retirement

- You want to leave tax-free money to heirs

SIMPLE IRA Strategy

SIMPLE IRA participants should always contribute enough to capture the full employer match, which is typically either a 2% non-elective contribution or a dollar-for-dollar match up to 3% of compensation. Beyond that, consider:

- Maximizing your SIMPLE IRA contributions if you don't have access to a 401(k) plan

- Taking full advantage of catch-up contributions if you're age 50 or older

- Utilizing the enhanced catch-up contributions if you're between the ages of 60 and 63

Take Action for 2026

With these increased limits taking effect in 2026, now is the perfect time to review your retirement savings strategy. Whether you contribute to a Traditional IRA, a Roth IRA, a SIMPLE IRA, or a combination of retirement accounts, understanding these changes helps you make informed decisions that align with your long-term financial goals.

At WealthRabbit, we're committed to helping you navigate these changes and optimize your retirement savings strategy. If you're looking for a more innovative way to manage your Traditional IRA, Roth IRA, or SIMPLE IRA, now is the perfect time to get started.

Start optimizing your retirement strategy today with WealthRabbit. Create your account and take the next step toward your financial future!

*This article is for informational purposes only and should not be considered tax or financial advice. Consult with a qualified tax professional or financial advisor to determine the best retirement savings strategy for your individual circumstances.