Traditional IRA vs. Roth IRA for 2026: A Comprehensive Guide

Choosing the correct retirement account is one of the most important financial decisions you can make, yet it is also one of the most misunderstood. Many savers open an IRA without fully understanding how taxes, income limits, and withdrawal rules will affect them years or even decades later. Others delay contributing altogether because they are unsure which option fits their situation.

That is why understanding the differences between a Traditional IRA and a Roth IRA before contributing for 2026 is an essential step in building a confident, long-term retirement plan. Each account offers meaningful benefits, but those benefits apply at different stages of your financial life.

Why the Choice Between Traditional and Roth Matters

No one wants to enter a new year uncertain about whether they chose the correct retirement account or missed an opportunity to optimize their tax strategy. Retirement decisions are cumulative, and small choices made today can have a meaningful impact on long-term outcomes.

By reviewing how each IRA is taxed, who is eligible to contribute, and how withdrawals work, you can make informed decisions that align with both your current income and your future expectations. Taking the time to understand these options now helps reduce confusion later and ensures your retirement savings are structured intentionally rather than by default.

A Deeper Look at the Traditional IRA

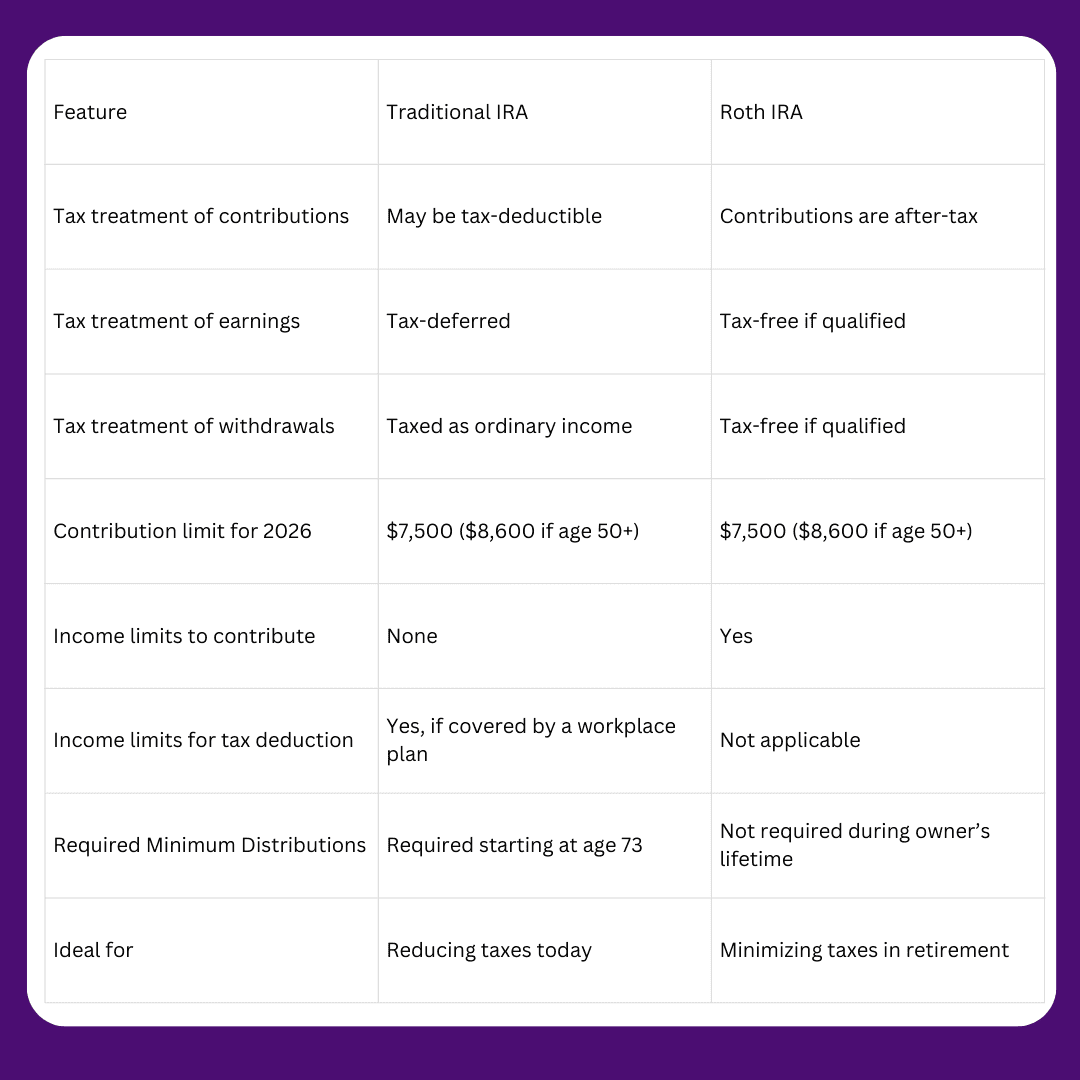

A Traditional IRA is designed to provide tax benefits in the present. Contributions may be tax-deductible, which can reduce your taxable income in the year you contribute. This feature makes Traditional IRAs especially appealing to individuals who are currently in higher tax brackets or who want to lower their tax bill while saving for retirement.

Contribution Limits and Eligibility for 2026

For 2026, you can contribute up to $7,500 to a Traditional IRA. If you are age 50 or older, you can make an additional $1,100 catch-up contribution, bringing your total contribution to $8,600. There is no maximum age limit for contributing, as long as you have earned income.

Anyone with earned income can contribute to a Traditional IRA, regardless of income level. However, the ability to deduct those contributions on your tax return may be limited if you or your spouse participates in a workplace retirement plan.

Deductibility Rules and Income Phase-Outs

If you are covered by a workplace retirement plan, such as a 401(k), the tax deductibility of your Traditional IRA contribution phases out based on income. For 2026, deductions phase out for single filers with incomes between $81,000 and $91,000, and for married couples filing jointly with incomes between $129,000 and $149,000.

If you are not covered by a workplace plan but your spouse is, the deduction for the non-covered spouse phases out between $242,000 and $252,000. These thresholds are important because they determine whether a Traditional IRA provides immediate tax savings or functions more like a tax-deferred savings vehicle without a deduction.

How Traditional IRA Growth and Withdrawals Work

Funds inside a Traditional IRA grow on a tax-deferred basis, meaning you do not pay taxes on dividends, interest, or capital gains in the year they are earned. Instead, taxes are deferred until money is withdrawn from the account. This allows investments to compound without annual tax drag, which can significantly increase long-term growth compared to taxable accounts.

Withdrawals from a Traditional IRA are taxed as ordinary income, regardless of whether the funds come from contributions or investment earnings. If withdrawals are taken before age 59½, they are generally subject to both ordinary income tax and a 10 percent early withdrawal penalty. However, the IRS allows specific exceptions to the penalty, including qualified higher education expenses, first-time home purchases up to a lifetime limit, certain medical expenses, disability, or substantially equal periodic payments. Even when penalties are waived, income taxes may still apply.

Once you reach age 73, Required Minimum Distributions must begin under the SECURE 2.0 Act, which increased the RMD starting age from 72 under prior law. Your first RMD must be taken by April 1 of the year following the year you turn 73, and all subsequent RMDs must be taken by December 31 each year. The required amount is calculated annually using IRS life expectancy tables and your account balance as of the prior year-end.

These mandatory withdrawals are designed to ensure that tax-deferred funds are eventually taxed. RMDs can meaningfully increase taxable income in retirement and may affect the taxation of Social Security benefits, Medicare premium surcharges, and eligibility for certain tax credits or deductions. Failing to take an RMD can be costly. Under current law, the penalty for missing an RMD is 25 percent of the amount not withdrawn, which may be reduced to 10 percent if the error is corrected promptly.

A Traditional IRA is often well-suited for individuals who expect to be in a lower tax bracket in retirement than they are during their working years or who place a high value on reducing taxable income during peak earning periods. However, the impact of future withdrawals and RMDs should be carefully considered as part of a broader retirement income strategy.

A Deeper Look at the Roth IRA

A Roth IRA offers a different type of tax advantage by focusing on future tax savings rather than immediate deductions. Contributions are made with after-tax dollars, meaning they do not reduce your current taxable income. In exchange, qualified withdrawals in retirement are completely tax-free.

Contribution Limits and Income Eligibility for 2026

Roth IRAs share the same contribution limits as Traditional IRAs. For 2026, you can contribute up to $7,500, or $8,600 if you are age 50 or older, as long as you meet the income requirements.

Eligibility to contribute depends on your modified adjusted gross income. Single filers with income under $153,000 can make a full contribution, with partial contributions allowed up to $168,000. Married couples filing jointly can make a full contribution of up to $242,000, with partial contributions allowed up to $252,000.

If your income exceeds these limits, you cannot contribute directly to a Roth IRA, although alternative strategies may be available with proper planning.

Roth IRA Growth, Withdrawals, and Flexibility

Like a Traditional IRA, funds in a Roth IRA grow without being reduced by annual taxes on earnings. The key difference comes at withdrawal. Qualified withdrawals, including earnings, are tax-free as long as the account has been open at least five years and you are at least age 59½.

Another defining feature of Roth IRAs is flexibility. Contributions, but not earnings, can be withdrawn at any time without taxes or penalties. While Roth IRAs are designed for retirement, this flexibility can provide peace of mind for savers who value access to their contributions.

Roth IRAs also do not require Required Minimum Distributions during the original owner’s lifetime. This allows assets to continue growing tax-free as long as they remain in the account, making Roth IRAs especially valuable for estate planning or for individuals who do not anticipate needing the funds immediately in retirement.

Strategic Considerations When Choosing an IRA

Choosing between a Traditional IRA and a Roth IRA often depends on when you expect to pay taxes and how predictable your future income will be. If your current tax rate is high and you expect it to be lower later, a Traditional IRA may provide greater overall tax efficiency. If your current tax rate is relatively low or you anticipate higher taxes in retirement, a Roth IRA may be more advantageous.

Some savers benefit from contributing to both account types over time. This approach creates tax diversification, allowing you to draw from taxable and tax-free sources in retirement and manage your income more strategically.

Planning Ahead with Confidence

By understanding how Traditional and Roth IRAs work and how the rules apply in 2026, you can move forward with clarity and confidence. Retirement planning is not about finding a single perfect choice, but about building a strategy that evolves with your income, goals, and life circumstances.

Ready to take control of your retirement? Sign up for a WealthRabbit account today and start managing your IRA with ease and confidence for 2026 and beyond.