Maximizing Your Retirement: Managing Multiple IRA Accounts the Smart Way

Having more than one retirement account can be a great way to maximize your savings and take advantage of tax benefits. But when you're juggling multiple IRAs—like a SEP and a Roth—it’s important to understand the contribution limits so you don’t accidentally over-contribute and get hit with penalties.

Here’s a simple breakdown of how multiple IRAs work, what the 2025 contribution limits are, and how to manage everything wisely.

Can You Have Multiple IRAs?

Yes! The IRS allows individuals to have multiple retirement accounts—even of the same type. For example, you can have both a SEP IRA and a Roth IRA, or multiple Traditional IRAs. However, annual contribution limits still apply across account types and exceeding them can result in penalties.

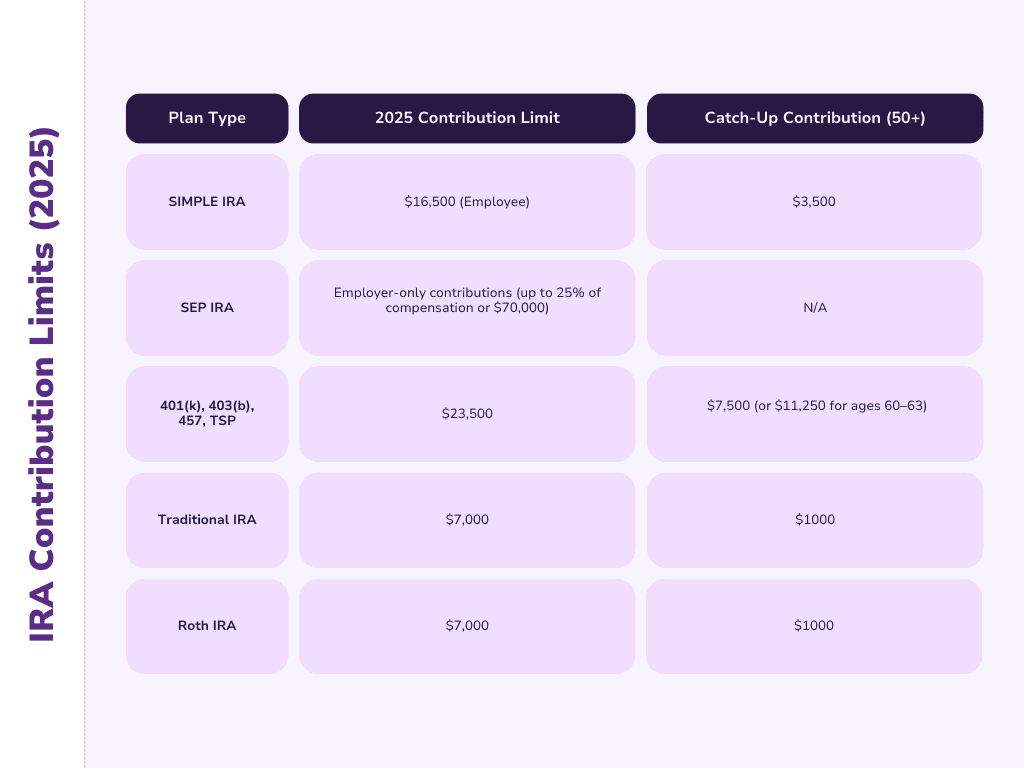

2025 Contribution Limits by Account Type

SIMPLE IRA

- Employee: $16,500 + $3,500 catch-up (for ages 50+)

- Employer: 3% match or 2% flat contribution

SEP IRA

- Employer-only contributions (up to 25% of compensation or $70,000)

- Self-employed? Use a modified formula based on net earnings (IRS Publication 560)

401(k), 403(b), 457, TSP

- $23,500 (under 50) + $7,500 catch-up (50+)

- Bonus catch-up of $11,250 for ages 60–63 under SECURE 2.0

Traditional & Roth IRA (Combined Limit)

- $7,000 total (under 50)

- $1,000 catch-up (50+)

Your total contributions across both accounts cannot exceed $7,000.

Tips for Managing Multiple Accounts

Having multiple accounts offers flexibility but requires planning and oversight. Here’s how to stay on track:

- Track contributions closely – Stay within limits to avoid IRS penalties

- Consolidate when possible – Fewer accounts mean simpler management

- Review annually – Rebalance your investments as your goals evolve

- Define a clear strategy – Know your long-term goals and risk tolerance

Example: Alex's Strategy with a SEP & Roth IRA

Alex is a freelance designer and small business owner. To make the most of her retirement savings, she opens:

- A SEP IRA for her self-employed income

- A Roth IRA for tax-free growth

Here’s what she contributes:

- $8,000 to her SEP IRA (within SEP limits based on her income)

- $6,500 to her Roth IRA (under age 50 limit for 2025)

Alex benefits from:

- Tax-deductible SEP contributions

- Tax-free Roth IRA withdrawals in retirement

But she stays smart by:

- Keeping SEP and Roth contributions separate (different rules!)

- Skipping a Traditional IRA to stay within the Roth/Traditional combined limit

- Checking her income to ensure Roth eligibility

Final Thoughts

Multiple retirement accounts can offer greater flexibility and long-term growth, but they come with more responsibility. Understanding each plan’s rules and limits helps you avoid penalties and make the most of your tax advantages.

WealthRabbit makes retirement planning easy, digital, and affordable for small businesses. Whether you're just getting started or managing a growing team, we’re here to help you stay compliant—and maximize every dollar.