The Backdoor Roth IRA: The Ultimate Guide for High Earners Who Exceed Roth Income Limits

You've heard about the Roth IRA. Tax-free growth. Tax-free withdrawals in retirement. No required minimum distributions. It sounds perfect, until you check the income limits and realize the IRS has basically put a velvet rope in front of one of the best retirement accounts in existence.

But here's the thing: that velvet rope has a back door.

The Backdoor Roth IRA is a completely legal strategy that lets high-income earners sidestep those income limits and still contribute to a Roth IRA. It's not a loophole - it's a perfectly legal strategy explicitly allowed by the IRS. It's a two-step process that's been around for years, used by millions of Americans, and is perfectly above board with the IRS.

This guide is going to walk you through everything: what it is, how it works, the tax traps to watch out for, and exactly how to set one up. Let's get into it.

New for this year: WealthRabbit has automated the Backdoor Roth process, making it easy for you to complete a backdoor Roth in just a few minutes. Click here to complete your Backdoor Roth today!

What Is a Backdoor Roth IRA?

A Backdoor Roth IRA isn't a special type of account. It's a strategy. Specifically, it's a two-step process where you:

- Make sure that you don’t have any balance in a traditional IRA, Simple IRA, or SEP IRA (or else the Backdoor Roth could be taxable - see the pro-rata rules later).

- Make a non-deductible contribution to a Traditional IRA (after-tax dollars, no tax break upfront)

- Convert that Traditional IRA to a Roth IRA

The reason it works is that while the IRS restricts who can contribute directly to a Roth IRA based on income, there's no income limit on Roth IRA conversions. Anyone, at any income level, can convert a Traditional IRA to a Roth IRA.

So the backdoor route lets you sneak in through the conversion door instead.

The result? Your money ends up in a Roth IRA, where it grows tax-free and can be withdrawn tax-free in retirement, even if you earn way too much to have contributed there directly.

Even a non-working spouse can use this strategy, as long as the household meets the earned income requirements based on the working spouse's income.

Roth IRA Income and Contribution Limits

Before we go further, let's talk about why the Backdoor Roth IRA exists in the first place: the income limits that lock high earners out of Roth IRAs.

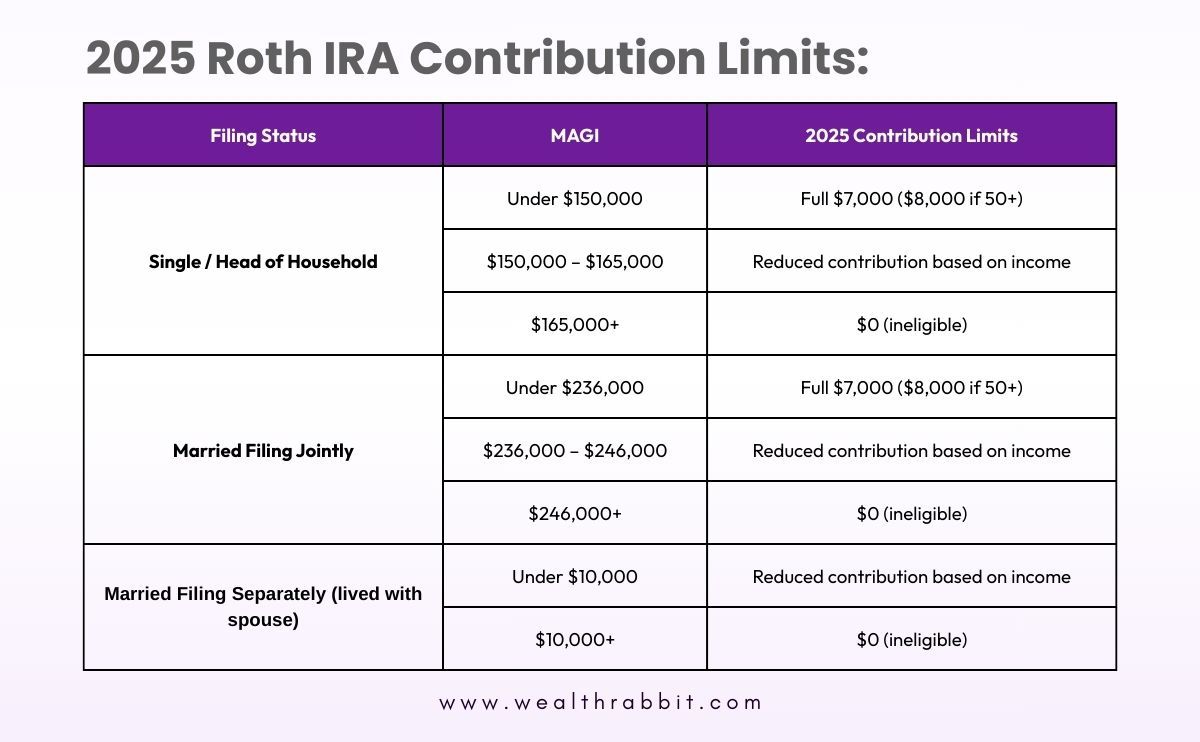

2025 Limits

For 2025, the Roth IRA contribution limit is $7,000 per year (or $8,000 if you're 50 or older). But your ability to contribute phases out based on your Modified Adjusted Gross Income (MAGI):

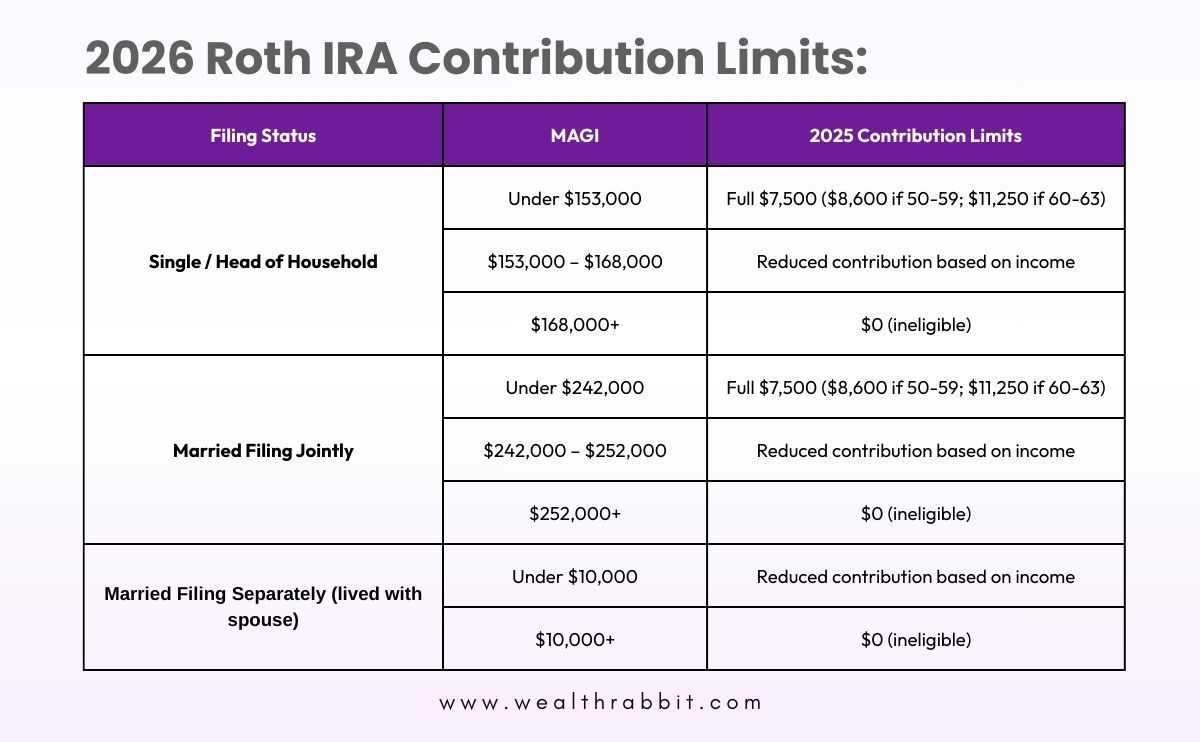

2026 Limits

The IRS has increased the contribution limit from $7,000 to $7,500(or $8,600 if you're 50 or older), and the income phase-out ranges shifted upward for 2026:

If your income puts you in the "$0" row, you literally cannot put money directly into a Roth IRA. That's exactly who the Backdoor Roth IRA strategy is built for.

The Advantages of a Backdoor Roth IRA

So why go through all the trouble? Because getting money into a Roth IRA is genuinely that valuable. Here's what you're gaining:

Tax-Free Growth. Once inside a Roth, your investments grow tax-free.

Tax-Free Retirement Income. Qualified withdrawals in retirement are 100% tax-free, unlike Traditional IRAs or 401(k)s.

No RMDs. Roth IRAs don’t force withdrawals at age 73, giving you full control over your money.

No Income Barrier. The backdoor strategy removes the income cap that blocks high earners from contributing directly.

Flexible Access. Withdrawals are tax and penalty-free once you reach age 59½ and have met the five-year holding requirement.

How Does the Backdoor Roth IRA Work?

Here's the step-by-step mechanics, and then we'll get into the tricky tax part that trips people up.

The Basic Two-Step Process

Step 1: Open a Traditional IRA and make a non-deductible contribution. This means you're contributing after-tax dollars. You don't claim a deduction on your taxes for this contribution. For 2025, you can contribute up to $7,000 ($8,000 if 50+).

Step 2: Convert that Traditional IRA to a Roth IRA. You transfer funds from a Traditional IRA to a Roth IRA. Since you already paid taxes on the money (it was a non-deductible contribution), you theoretically owe no additional tax on the conversion, assuming you do it quickly and the money hasn't earned any income in the meantime.

In the purest form of this strategy, you'd contribute and convert in 3 to 5 business days. No time for investment gains, minimal tax consequences.

But here's where it gets complicated.

The Pro-Rata Rule: The Tax Trap You Need to Know

The pro-rata rule is part of the Backdoor Roth strategy and can catch people off guard; it's critical to understand before taking any action.

The IRS treats all your Traditional IRAs as one combined account when calculating taxes on a conversion. It doesn't matter if the money is in ten different accounts at different institutions. For tax purposes, they're treated as a single unit.

When you convert any portion of a Traditional IRA to a Roth IRA, the IRS requires that you treat the conversion as coming proportionally from all of your Traditional IRA money, both the pre-tax money (deductible contributions and earnings) and the after-tax money (your new non-deductible contribution).

Here's the formula the IRS uses:

Taxable % = (Total Pre-Tax IRA Balance ÷ Total IRA Balance) × 100

This ratio determines what percentage of your conversion is taxable. Let's walk through all three scenarios.

Scenario 1: All After-Tax Money (The Clean Backdoor)

This is the ideal scenario. You have no existing Traditional IRA balances from pre-tax contributions. Your only IRA money is the fresh non-deductible contribution you just made.

Example: You open a new Traditional IRA and contribute $7,500 in after-tax dollars. You have no other IRAs. You convert immediately to a Roth IRA.

- Total IRA balance: $7,500

- Pre-tax portion: $0

- After-tax portion: $7,500

Pro-rata calculation: $0 ÷ $7,500 = 0% taxable

Result: You pay zero tax on the conversion. The entire $7,500 moves into your Roth IRA tax-free. This is the backdoor working exactly as intended, clean, simple, and tax-efficient.

The only caveat: if your $7,500 earns even a small amount before you complete the conversion (say, $15 in interest), that $15 will be taxed as ordinary income. This is why most people recommend converting as quickly as possible after contributing.

Scenario 2: Existing Pre-Tax IRA Balances

This is where things get messy. If you already have a Traditional IRA funded with pre-tax dollars (deductible contributions or rolled-over 401(k) funds), the pro-rata rule will make your "clean" backdoor conversion much less tax-efficient.

Example: You have a $50,000 rollover IRA from an old 401(k), all of which is pre-tax money. You open a new Traditional IRA and make a $7,500 non-deductible contribution. Now you have two IRAs totalling $57,500.

You go ahead and convert just that new $7,500 into a Roth IRA.

The IRS doesn't let you say "I'm only converting the new after-tax money." Instead, it applies the pro-rata rule:

- Total IRA balance: $57,500

- Pre-tax portion: $50,000

- After-tax portion: $7,500

- Taxable percentage: $50,000 ÷ $57,500 = 86.9%

So even though you're only converting $7,500, roughly 86.9% of that (about $6,517) is considered taxable income in the year you convert.

Instead of a clean, tax-free conversion, you're adding $6,517 to your taxable income. Depending on your tax bracket, that could be a meaningful tax hit. And you still only got $983 worth of after-tax money into your Roth.

This is why the backdoor strategy doesn't work well for people who already have large pre-tax Traditional IRA balances.

Scenario 3: Capital Gain Scenario

Let's add another layer: what if you invest your non-deductible contribution and the account grows before you convert?

Example: You contribute $7,500 to a Traditional IRA in non-deductible dollars. You invest it in an S&P 500 index fund. A week later, your IRA is worth $7,575 due to market movement. You now convert to a Roth IRA.

Even if there are no existing pre-tax IRA balances, that $75 gain is taxable. The IRS considers investment gains to be pre-tax money (since you never paid tax on the earnings), so:

- After-tax basis: $7,500

- Taxable gain: $75

- Total converted: $7,575

- Taxable amount: $75 (taxed as ordinary income

The key rule: Any amount converted from a Traditional IRA that represents pre-tax dollars or earnings will be taxed as ordinary income in the year of conversion. Capital gains rates don't apply here. It's all ordinary income.

Backdoor Roth IRA Tax Implications

Let's consolidate the key tax considerations you need to be aware of.

The December 31 Rule

Here's a timing detail that trips people up: the IRS calculates the pro-rata ratio based on your total IRA balance on December 31 of the tax year in which you do the conversion, not on the day you convert.

This is huge. Here's why it matters:

Example: You have a $100,000 rollover IRA sitting in a Traditional IRA. In November, you contribute $7,500 in non-deductible dollars to a separate Traditional IRA and immediately convert it to a Roth. At the time of conversion, your math looks great, just the $7,500 account.

But the IRS looks at December 31 of that same year. If your $100,000 rollover IRA is still sitting there on December 31, the pro rata rule applies to your conversion, retroactively based on that combined balance ($107,500).

Your "clean" conversion suddenly becomes 93% taxable because the IRS sees $100,000 in pre-tax IRA money on the last day of the year.

The 10% Early Withdrawal Penalty and the 5-Year Rule

The Backdoor Roth IRA involves a conversion, and conversions have their own 5-year clock. Here's how it works:

Each Roth conversion starts its own separate 5-year holding period. If you withdraw converted funds from your Roth IRA within 5 years of that specific conversion, and you're under age 59½, you could face a 10% early withdrawal penalty on the converted amount.

Note that this applies to the converted principal (the money you already paid taxes on), not just the earnings. So if you convert $7,000 in year one and withdraw it in year two because you need cash, you may owe a 10% penalty ($700) even though you already paid income tax on it.

IRS Form 8606: You Must File This

Every time you make a non-deductible contribution to a Traditional IRA, you must file IRS Form 8606 with your tax return. This form tracks your "basis," which is the after-tax money you've put into your IRAs.

Without Form 8606:

- The IRS has no record that your contribution was non-deductible

- You could end up paying taxes twice on the same dollars when you eventually convert or withdraw

- You lose the paper trail that protects you

You'll also receive a Form 1099-R from your financial institution when you do the conversion. This reports the distribution from your Traditional IRA. You use this together with Form 8606 to properly report the conversion on your tax return.

Bottom line: don't skip Form 8606. File it every single year you make a non-deductible IRA contribution, even if nothing else changes.

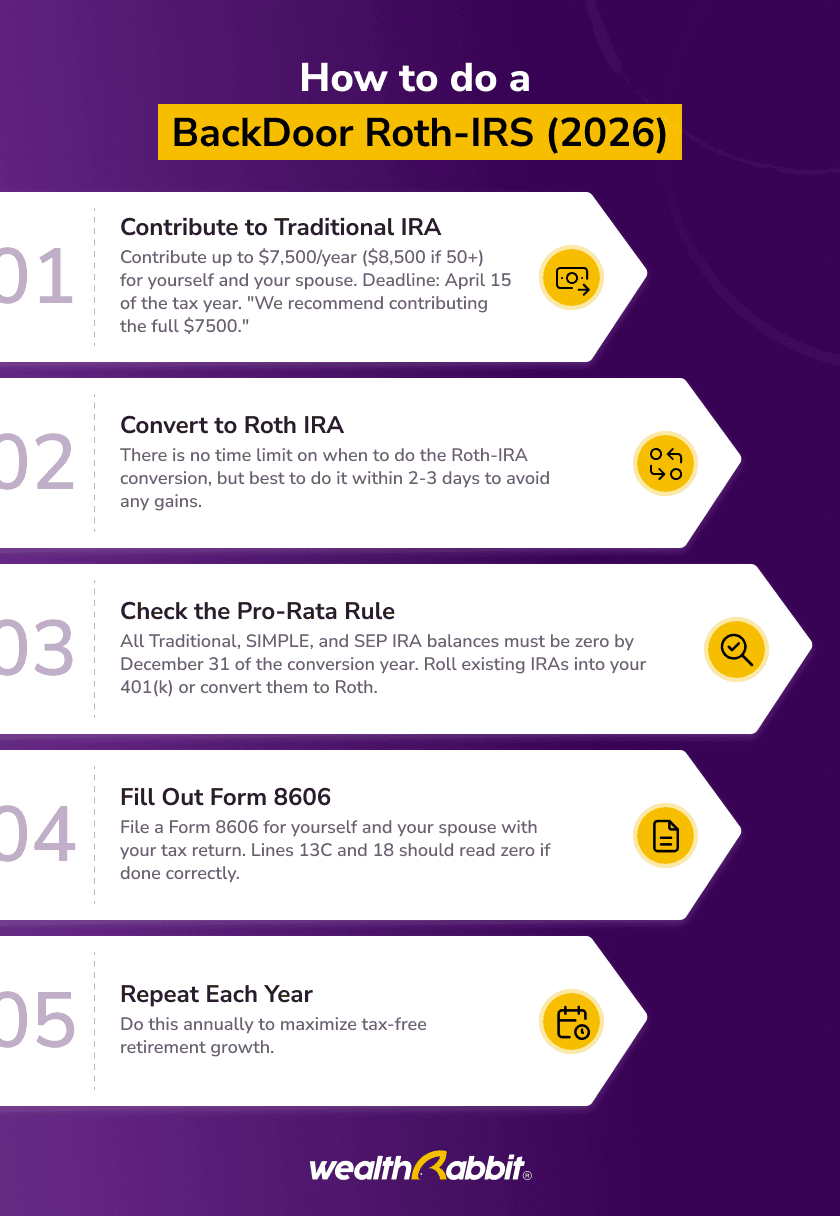

How to Set Up a Backdoor Roth IRA: Step-by-Step

Step 1: Check for Existing Pre-Tax IRA Balances

Before anything else, inventory all your Traditional IRA accounts, SEP-IRAs, and SIMPLE IRAs. Add up the total pre-tax balances across all of them. If you have significant pre-tax balances, consider rolling them into a current employer 401(k) before proceeding. This will help you sidestep the pro-rata rule.

Step 2: Open a Traditional IRA (If You Don't Have One)

Open a Traditional IRA. Make sure it's a Traditional IRA, not a Roth.

Step 3: Make a Non-Deductible Contribution

Contribute up to the annual limit:

- 2025: $7,000 (ages under 50), $8,000 (ages 50-59), $10,000 (ages 60-63)

- 2026: $7,500 (ages under 50), $8,600 (ages 50-59), $11,250 (ages 60-63)

When you file your taxes, you will not claim a deduction for this contribution. Keep the money in cash or a money market fund while it's in the Traditional IRA. Don't invest it in equities yet, as you want to avoid gains before the conversion. Any investment earnings that occur before conversion will be taxed as ordinary income.

Step 4: Wait for the Funds to Settle

After you contribute, there's typically a short settlement period, often just a few business days. Your brokerage will let you know when the funds are available for a conversion. Some institutions have a 7-day hold, so check your custodian's specific policy.

Step 5: Convert to a Roth IRA

Once the funds have settled, initiate the conversion to your Roth IRA. If you don't already have a Roth IRA open at the same institution, you'll need to open one. Some brokerages require both accounts to be held with them to do the conversion directly. Otherwise, you may need to do an indirect rollover, which adds complexity.

Convert the full balance to keep things clean and avoid future complications.

Step 6: Report it on Your Taxes

This is where most people get confused, so let's be very clear about what you need to do:

File Form 8606: Part I records your non-deductible Traditional IRA contribution and tracks your after-tax basis. Part II reports the conversion to Roth and calculates how much is taxable using the pro-rata formula.

Report Form 1099-R: Your brokerage will send you this form after the conversion. It shows the amount distributed from the Traditional IRA. You'll include this on your tax return.

Work with a tax professional if this is your first time doing a backdoor conversion, or if you have existing pre-tax IRA balances that complicate the pro-rata calculation.

Step 7: Invest the Money in Your Roth IRA

Once the conversion is complete and the money is sitting in your Roth IRA, invest it according to your retirement strategy. Now it's in the tax-free zone. Time to let it grow.

Conclusion

The Backdoor Roth IRA is one of the best moves a high-income earner can make for their retirement. Watch your pre-tax IRA balances because of the pro-rata rule, convert quickly after contributing, and file Form 8606 every single year. Do those things right, and you've got a tax-free growth engine working for you for decades.

The back door is open. And with WealthRabbit, walking through it takes minutes, not months

Ready? WealthRabbit Makes It Simple.

WealthRabbit is proud to provide the first automated Backdoor Roth strategy. We do all the heavy lifting, making it easy for you to do a Backdoor Roth in a few minutes.

Here's what makes WealthRabbit different:

- Open both your Traditional IRA and Roth IRA in one application

- Make your non-deductible contribution

- Authorize automatic conversion

- We convert within 3-5 business days automatically

- Get email confirmations at every step

- Both accounts live on one platform—no transfers between brokerages

- No manual tracking. No missed conversions.

Everything is handled in one seamless flow. You authorize it once. We take it from there.

Start your Backdoor Roth IRA with WealthRabbit today

Related Blog Posts

--No related posts available--