Why SIMPLE IRA Make Sense for Your Small Business

That's the real story behind SIMPLE IRAs. They were built specifically for businesses that don't have an HR department, a benefits team, or hours to spare on plan administration. If you're running a business with 100 or fewer employees, this is one of the few retirement plans that actually fits the size of your operation instead of forcing you to grow into it.

What a SIMPLE IRA Actually Is

SIMPLE stands for Savings Incentive Match Plan for Employees, which is a mouthful for something that's genuinely straightforward. Employees set aside a portion of their paycheck pre-tax, and you, the employer, kick in a contribution too. That's it. No nondiscrimination testing, no Form 5500 filing in most cases, no plan document drafted by a benefits attorney charging by the hour.

For 2026, employees can defer up to $17,000 a year, with an extra $4,000 catch-up if they're 50 or older (and a higher $5,250 catch-up for those 60 to 63). If your business has 25 or fewer employees, the IRS lets you offer even higher limits, up to $18,100 in deferrals.

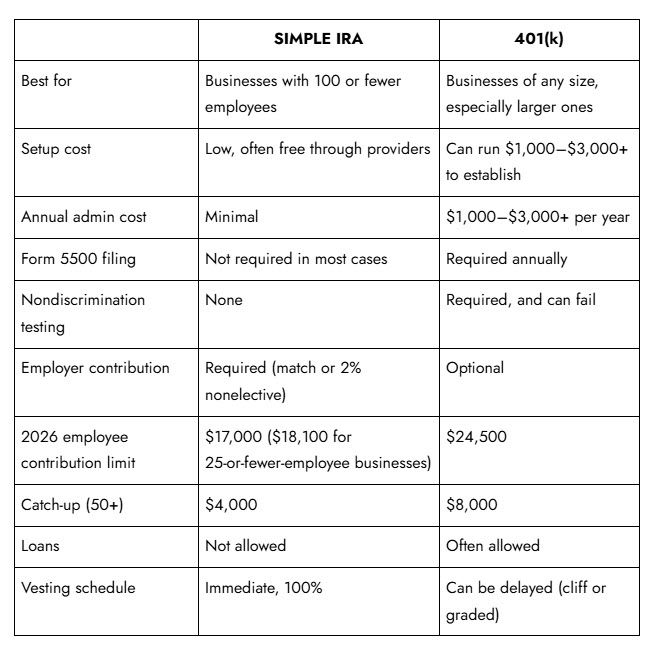

SIMPLE IRA vs. 401(k): A Side-by-Side Look

The honest answer to "which one should I pick" usually comes down to size and budget. Here's how they stack up.

That vesting row deserves its own beat. With a SIMPLE IRA, every dollar you put in belongs to the employee immediately. No "you have to stay three years to keep it." For a small business trying to compete with bigger companies on benefits, that's a real selling point when you're recruiting, not just a compliance detail. It's a fair trade, though. You're getting simplicity and lower cost in exchange for lower contribution limits and no loan provisions. If your team is bumping up against the $17,000 ceiling every year, that's actually a signal you may have outgrown the SIMPLE IRA and should start looking at a 401(k).

Why the Trade-Off Works in Your Favor

A 401(k) is a great plan once you have the payroll team and budget to support it. But for a business with a handful of employees, the cost and complexity often outweigh the benefit. SIMPLE IRAs flip that math.

You have two ways to contribute as the employer: match employee contributions dollar-for-dollar up to 3% of their pay, or make a flat 2% nonelective contribution to every eligible employee whether they contribute or not. Either way, you know your cost ahead of time. There's no surprise testing failure that forces you to refund contributions to highly compensated employees, which is a real headache that trips up small 401(k) plans more often than people expect.

This is one of those cases where doing the responsible thing and doing the easy thing happen to be the same thing. You're not choosing between simplicity and a real benefit. You get both.

The Part That Actually Trips People Up

Here's the part nobody mentions in the pitch: setting up a SIMPLE IRA isn't hard, but staying compliant with it is where small business owners quietly fall behind. You need to give employees written notice before the plan year starts, get the IRS forms filed correctly (5304-SIMPLE or 5305-SIMPLE depending on whether employees choose their own provider), make sure payroll deductions are calculated right every single cycle, and meet contribution deposit deadlines that the IRS does not treat casually.

None of this is complicated in isolation. But it adds up, especially if you're already doing your own bookkeeping, your own payroll, and trying to run the actual business in the time left over.

Where WealthRabbit Fits In

This is exactly the gap WealthRabbit was built to close. Instead of juggling notice deadlines, contribution calculations, and IRS paperwork across spreadsheets and sticky notes, WealthRabbit gives accountants and CPA firms a single place to set up and manage SIMPLE IRA plans for their small business clients, with the compliance tracking built in instead of bolted on.

If you're a business owner reading this, talk to your accountant about WealthRabbit. If you're the accountant, you already know how many client hours go into manual SIMPLE IRA administration every year, and you know exactly what getting that time back would mean for your practice.

A SIMPLE IRA was already the easy choice. WealthRabbit just makes sure it stays that way.

Related Blog Posts

--No related posts available--