SEP IRA vs. SIMPLE IRA: A Guide for Small Business Retirement Planning

As a small business owner, offering a retirement plan is a smart way to attract and retain employees, reduce taxable income, and secure your own financial future. But with multiple options available, it can be challenging to determine the best fit. Two of the most common retirement plans for small businesses are SEP IRAs (Simplified Employee Pension Plan) and SIMPLE IRAs (Savings Incentive Match Plan for Employees).

Both plans offer tax advantages, easy setup, and lower costs compared to a traditional 401(k), but they serve different business needs. This guide will break down the key differences and help you determine which one is right for your business.

What is a SEP IRA?

A SEP IRA is a tax-deferred retirement plan designed for self-employed individuals and small business owners. It allows employers to contribute to their own retirement savings as well as to their employees’ accounts.

Key Features of a SEP IRA:

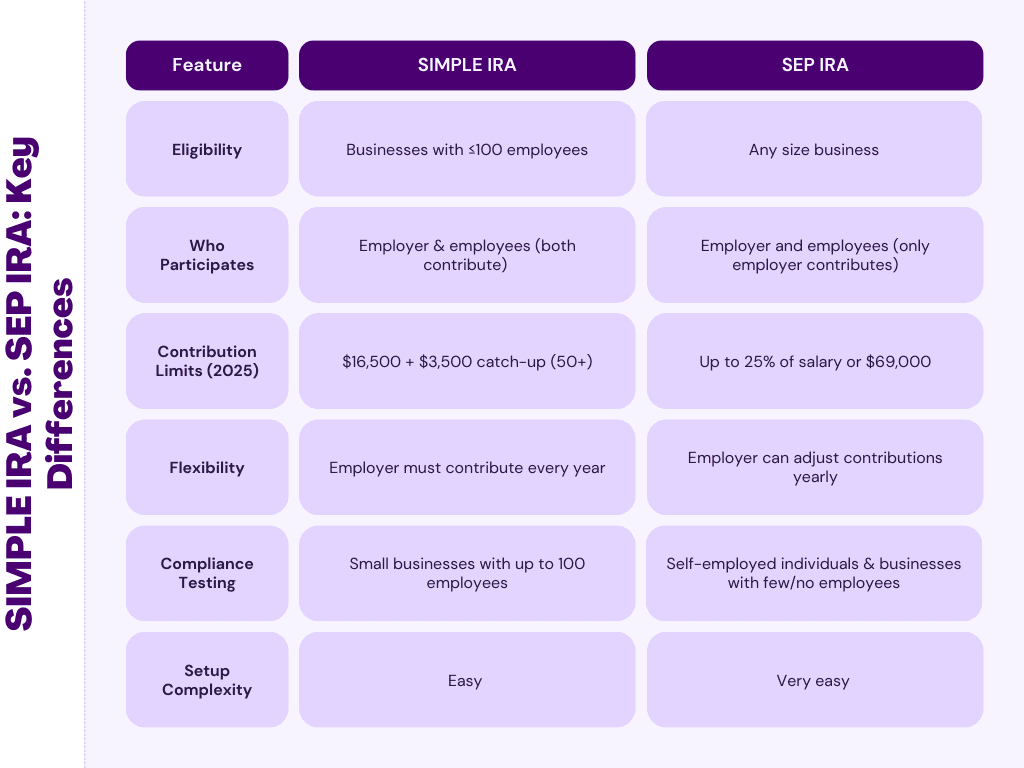

- High contribution limits – Employers can contribute up to 25% of an employee’s salary or $69,000 in 2024, whichever is lower.

- Employer-funded only – Employees cannot contribute; only the employer makes contributions.

- Flexible contributions – Employers can adjust contributions each year based on business performance.

- Easy setup & low maintenance – Fully digital experience, no annual IRS filing, and no complex compliance testing.

- Tax advantages – Contributions are tax-deductible, reducing the business’s taxable income.

Best for:

- Self-employed individuals or businesses with few or no employees.

- Companies with fluctuating profits that want the flexibility to adjust contributions each year.

- Business owners looking for higher contribution limits than a SIMPLE IRA.

What is a SIMPLE IRA?

A SIMPLE IRA is a retirement plan specifically designed for businesses with 100 or fewer employees. It provides an easy, low-cost way for both employers and employees to save for retirement.

Key Features of a SIMPLE IRA:

- Lower contribution limits – Employees can contribute up to $16,000 in 2024 (or $19,500 if age 50+).

- Employer contributions required – Employers must either:

- Match up to 3% of each participating employee’s salary, OR

- Make a fixed 2% contribution for all eligible employees, regardless of participation.

- Employee participation – Employees can make pre-tax contributions to their accounts.

- Easier & cheaper than a 401(k) – No complex compliance testing or expensive administration.

- Tax advantages – Employer contributions are tax-deductible, and employee contributions grow tax-deferred.

Best for:

- Small businesses with employees who want to contribute to their own retirement savings.

- Companies looking for a structured plan with required employer contributions.

- Business owners who prefer a simple, low-maintenance alternative to a 401(k).

Let's Compare

How to Choose the Right Plan

The best choice depends on your business size, structure, and financial goals.

1. Choose a SEP IRA if you’re self-employed or have a few employees and want the flexibility to contribute large amounts in good years and reduce contributions in slow years.

2. Choose a SIMPLE IRA if you have multiple employees who want to contribute to their own retirement and you’re comfortable with the mandatory employer contribution.

Both plans are cost-effective alternatives to a traditional 401(k), offering significant tax advantages and simplified administration.

Still not sure? WealthRabbit has answers!

Get Started with the Right Plan Today

Choosing a retirement plan doesn’t have to be complicated. WealthRabbit makes it easy to set up and manage a SEP IRA or SIMPLE IRA with automated contributions, compliance tracking, and a user-friendly platform.

Explore your options and start building a secure financial future for your business today.